Weighed On By Its Debt Load?")

Legendary fund supervisor Li Lu (who Charlie Munger backed) once reported, ‘The greatest expense threat is not the volatility of price ranges, but whether or not you will go through a everlasting reduction of money.’ It truly is only all-natural to take into account a company’s equilibrium sheet when you look at how risky it is, because debt is usually concerned when a business enterprise collapses. As with quite a few other businesses China Facts Know-how Enhancement Minimal (HKG:8178) will make use of personal debt. But really should shareholders be nervous about its use of personal debt?

When Is Credit card debt Harmful?

Personal debt is a tool to help enterprises mature, but if a company is incapable of paying off its loan providers, then it exists at their mercy. Ultimately, if the enterprise cannot fulfill its authorized obligations to repay credit card debt, shareholders could walk away with very little. While that is not far too prevalent, we generally do see indebted companies completely diluting shareholders mainly because lenders pressure them to raise funds at a distressed selling price. Of program, a good deal of companies use debt to fund advancement, without the need of any negative implications. The initially issue to do when looking at how considerably personal debt a organization works by using is to glimpse at its dollars and financial debt with each other.

Test out our most recent examination for China Info Know-how Enhancement

What Is China Info Technologies Development’s Web Financial debt?

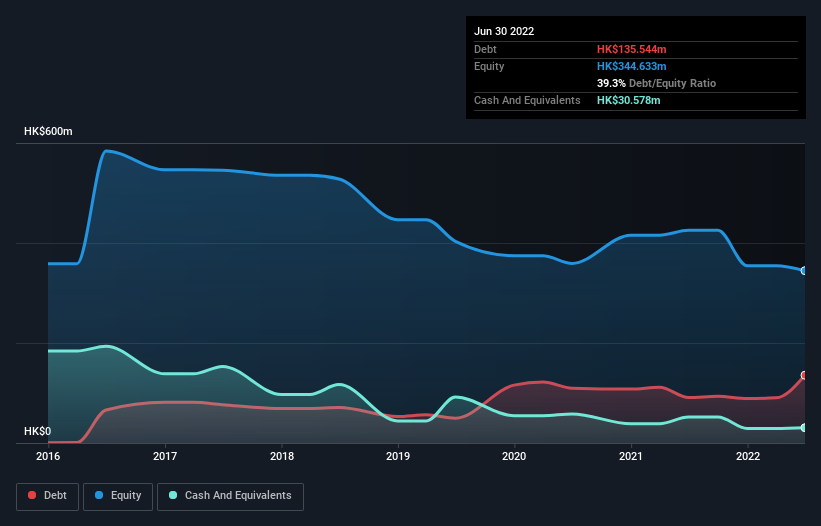

As you can see under, at the finish of June 2022, China Facts Know-how Enhancement experienced HK$135.5m of financial debt, up from HK$91.0m a calendar year in the past. Click the graphic for much more detail. On the other hand, due to the fact it has a money reserve of HK$30.6m, its net financial debt is much less, at about HK$105.0m.

How Potent Is China Details Engineering Development’s Harmony Sheet?

Zooming in on the hottest harmony sheet knowledge, we can see that China Data Technologies Enhancement experienced liabilities of HK$87.4m owing in 12 months and liabilities of HK$84.4m owing outside of that. Offsetting these obligations, it had money of HK$30.6m as very well as receivables valued at HK$42.9m because of in just 12 months. So it has liabilities totalling HK$98.3m extra than its money and close to-term receivables, put together.

Provided this deficit is basically bigger than the company’s market capitalization of HK$81.8m, we believe shareholders definitely should really observe China Details Know-how Development’s financial debt concentrations, like a dad or mum watching their youngster trip a bike for the very first time. Hypothetically, particularly major dilution would be essential if the company had been forced to shell out down its liabilities by boosting capital at the recent share price tag. The equilibrium sheet is obviously the space to target on when you are analysing personal debt. But you cannot see debt in overall isolation considering that China Info